ACH vs Wire Transfers

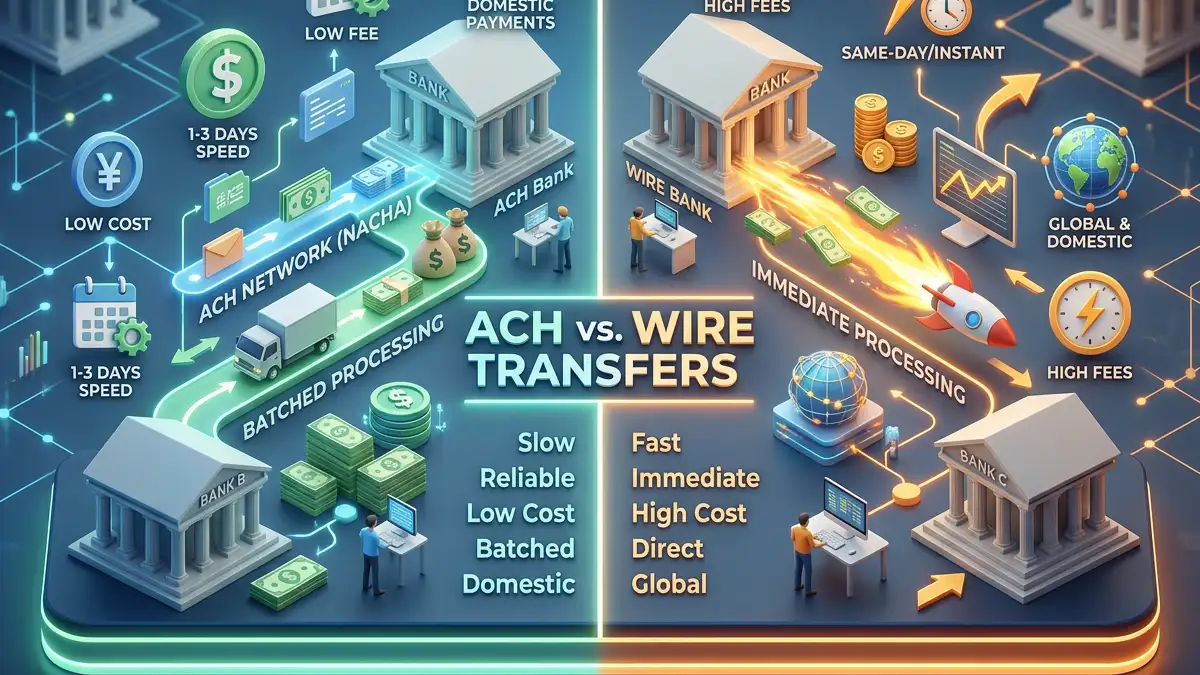

Graphic showing the various differences between Wire and ACH transfers

Credit: Adaptiv Payments

Tech Lead at Adaptiv Payments | More

What Is an Automated Clearing House (ACH) Transfer?

ACH transfers are batched bank-to-bank transactions processed through the Automated Clearing House Network. They are commonly used for B2B invoices, peer-to-peer lending, direct deposit payouts, and bank payments.

ACH is primarily a U.S. rail, as international companies use different systems. If you work primarily in the United States, an ACH merchant account can meet your needs.

What Is a Wire Transfer?

A wire transfer is a secure electronic payment between different bank or credit union accounts. Unlike ACH transfers, wire transfers are common for cross-border transactions, provided through services like SWIFT, Wise, or Western Union.

They are ideal for urgent payments because of their speed, and are often used for high-value payments like down payments because they are harder to reverse once sent. Wire transfers are processed individually, meaning they have additional fees.

Differences Between ACH Transfers and Wire Transfers

While ACH transfers and wire transfers are both electronic fund transfers, there are key differences between them.

ACH payments typically take several days to process, though they are affordable and reversible. International ACH transfers are not common because the network is mostly in the US.

Wire payments are the preferred option for transferring funds internationally, but wire transfer fees are higher than for ACH transactions. Wire transfers are also harder to reverse, meaning you must be sure of the recipient's identity.

| ACH Transfers | Wire Transfers | |

|---|---|---|

| Speed | A few business days, though same-day ACH is possible | Typically same-day processing |

| Fees/Cost | Lower fees | Higher fees |

| Reversibility/Finality | Reversible | Difficult to reverse |

| Fraud risk pattern | Low risk; easy to reverse transactions | High risk; wire fraud is difficult to reverse |

| Best use cases | Recurring bills, routine payments to a known company | Time-sensitive and high-value payments, international transactions |

| Domestic vs. international fit | Domestic transfers | International transfers |

| Reconciliation and recordkeeping notes | Batched transfers require reconciliation against one settlement amount | For international wires, they must reconcile currency changes |

Reversibility and Disputes Involving ACH or Wire Transfers

While ACH is valuable for recurring payments and everyday transactions, there are dangers to using e-checks. One common issue is when the sender's account has insufficient funds, especially if the receiving bank takes a few days to process the transfer. Banks charge a returned check fee, endangering your cash flow.

ACH allows returns and unauthorized payment disputes, meaning you will need to have a process in place to handle returns or insufficient funds issues.

Wire transfers are very difficult to reverse once initiated, especially cross-border wire transfers. If you choose to transfer money for vendor payments or large-ticket items, ensure you have network security and confirm the recipient's account information before sending funds.

How ACH and Wire Transfers Differ From Cards in Terms of Fraud and Chargebacks

ACH and wire transfers have different processes for fraud and chargebacks, making it crucial to choose the right payment method based on the risk of fraud.

- Credit and Debit Cards: Cardholders can initiate a dispute, which allows the issuing bank to reclaim funds from the merchant account.

- ACH: These are initiated when the transfer cannot be completed, such as due to a return or an unauthorized claim. It has a different workflow than card chargebacks, with the receiving bank issuing a return code to the originating bank.

- Wire Transfers: These direct transfers generally do not have a chargeback rail. Fraud tends to be misdirection, like sending to the wrong bank account, or social engineering. Recovery is difficult and requires clear evidence of fraud, meaning that senders should be cautious and double-check all details.

Choosing a payment services provider with strong fraud protection features adds extra protection when sending money electronically, including real-time monitoring and fraud alerts.

Best Use Cases for Wire Transfers and ACH Payments

Infographic showing the differences between ACH and wire transfers.

Credit: Adaptiv Payments

It's common for merchants to use both wire transfers and ACH transfers depending on the specific transaction, including the ticket value, whether it is recurring or one-time, and the recipient's geographic area. Consider these use cases to decide which one is right for this particular transaction.

Wire Transfers

- Very high-value payments, like car down payments

- Urgent payments

- International payments

- Large travel deposits, like for luxury cruises

- High-value contracting work, such as large-scale commissions

ACH Transfers:

- Low-fee B2B invoices

- Routine contractor or affiliate payouts

- Monthly subscriptions with low return risk

- Domestic payments

- Ecommerce payments

- Low-value travel deposits with delayed fulfillment

- Bank-pay for high-ticket, domestic purchases

How Merchants Should Choose the Right Option

Choosing between ACH and wire transfers depends on your customer type, product, and overall business model.

- Customer Type: Everyday consumers are not very familiar with wire transfers, or they associate them with Western Union scams. They may also not be willing to pay the additional transfer fees. Business buyers understand the benefits of wire transfers, particularly that they are not easily reversed, and may prefer this for larger transactions.

- Product Type: Digital products have higher dispute patterns, but also clearer proof of delivery, making them suitable for ACH transfers. Wire transfers are suitable for very high-value physical items with clear proof of delivery, such as fine art, cars, or houses. Because wire transfers are not easily reversed, you will need clear documentation to avoid disputes.

- Fulfillment Timing: You should also consider whether you have immediate fulfillment or delayed fulfillment, as this changes the risk of returns or disputes. ACH is suitable for delayed fulfillment, as it is reversible if the buyer cancels or disputes the quality. Wire transfers are better for a high-value, immediate fulfillment, where the buyer can verify quality and is unlikely to dispute the claim.

- Ticket Size: ACH transfers are batched after a simple verification, making them more suitable for low-ticket items. For high-ticket items, wire transfers are a preferable choice, as they undergo manual review before being approved.

- Geography: While international ACH transfers are sometimes possible, they may be slower and incur higher fees. ACH is best for domestic use cases, as the network is set up to operate in the United States. Wire transfers are preferred for cross-border use because there is a network of financial institutions that handles cross-border wire transfers.

- Operational Capacity: ACH returns and reconciliation are a significant aspect of using the service, meaning you must have accounting software that can reconcile batched settlements with transactions. Wire transfers are generally non-returnable and processed individually, making them preferred for one-time large-sum transfers.

High-Risk Merchants Need Multiple Rails

Having a blend of payment options available to you ensures that you can match the transaction risk profile and customers' needs without incurring high fees. However, high-risk merchants often struggle to get approved by traditional financial institutions due to complex regulations, high chargeback rates, or fraud risk. This is why thousands of merchants in industries like travel, CBD, or ecommerce choose alternative payment service providers that better meet their needs.

Adaptiv Payments provides quality merchant accounts and payment processing for high-risk industries with competitive rates and comprehensive customer support. Our industry specialists understand your industry's needs and provide a personalized underwriting process tailored to your business model.

With Adaptiv Payments, you receive a flexible merchant account with built-in fraud protection and chargeback mitigation. We use PCI-DSS-compliant security measures, including 3D Secure, tokenization, and encryption, to keep customer data safe at all times. Our integrations enable you to provide a seamless payment experience for customers on most ecommerce platforms.

Whether you need to manage an international team of freelancers, process payments from multiple platforms, or integrate ecommerce sales with your brick-and-mortar store, Adaptiv Payments' all-in-one payment services ensure that you're ready to build your business. Contact us today for a free quote.

FAQs

Yes, ACH transfer fees are lower. They are batched, meaning that one bank gathers all its transfers and sends them out at once rather than sending payments one by one. This makes them a low-cost option for routine transactions. In contrast, wire transfers are processed individually and often manually reviewed before approval. While this makes them a secure payment option for high-ticket transactions, it also means additional fees.